David Beisel

*This post is part of our “pitch deck” series where we dissect the seed stage pitch deck and discuss the ideal flow for a pitch. You can read the rest of the posts in the series by clicking here*

Download Full Template Here

For many pitch decks, the Appendix section is really an afterthought. It contains rejected slides which didn’t quite fit into the main deck and half-baked ideas which aren’t fully thought-through. Alternatively, quite a few decks don’t even have an Appendix at all. These scenarios shouldn’t be the case. At NextView, we believe that the pitch deck isn’t over with the “last ask” slide. Instead, the Appendix should be used strategically.

The Appendix is a gift in that it can include meaningful material with little concern about the length or where it fits into the overall story, so it’s a section to really take advantage of. Philosophically, the main deck should be as succinct as possible in sharing a story arc.

Thought of in conjunction, the appendix then can become the “kitchen sink” of everything that a potential investor might ask about or want to know that didn’t fit into the short story of the main section.

For example, there are some slides which an investor requires, like a financial projection model or an extensive competitor analysis which don’t necessarily make sense in a primary section, as they could add friction to telling an actual story. Plus, every business is different, and so it’s best to think about all of the questions that a new investor could potentially ask so during a pitch meeting you can respond with, “I’ve prepared as slide on that topic.”

Having a slide on key questions to refer back to demonstrates and signals that you as the Founder have critically thought about all aspects of your business, not just haphazardly created a top-level pitch deck.

A few potential slides which can be included in the Appendix:

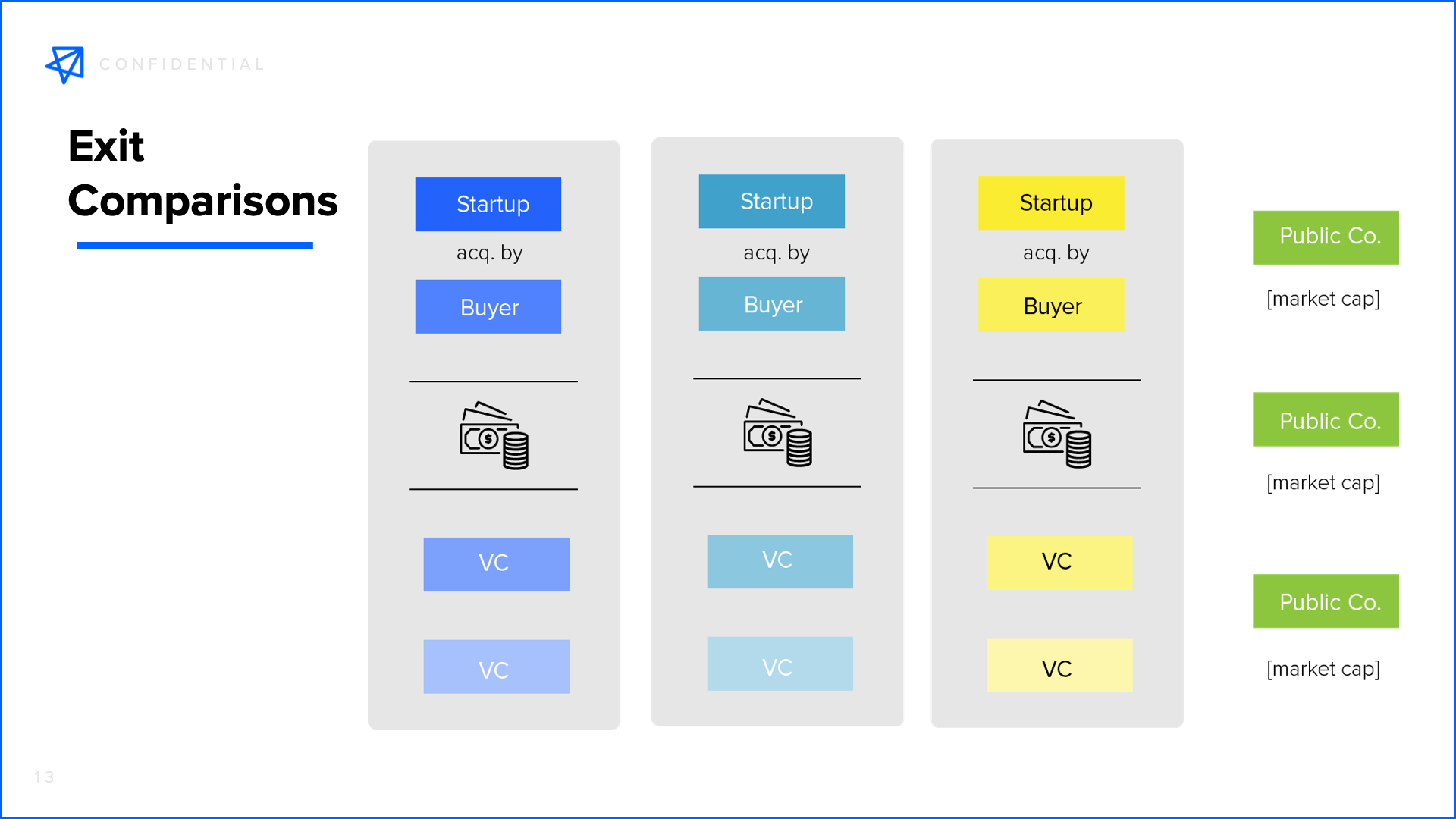

Exit Analysis: Not always as important during the early startup stage since an exit event is presumably in the distance away. Along those lines, there is risk that too much devoted materials & airtime to this subject could signal Founder impatience looking for a “quick win” rather than the excitement to build for the next decade towards a monster-scale outcome, so including a slide on the topic an the Appendix is the perfect place for it.

A slide looking at comparable exits and/or potential acquirers can be especially useful for ventures which don’t neatly fit into a specific category or bucket.

Something standard like a SaaS company where the exits scenarios and valuations are well-understood may not need a slide here, but the more non-traditional or unique the venture is, the more information which a Founder can fill in the blanks of “what could be” are helpful.

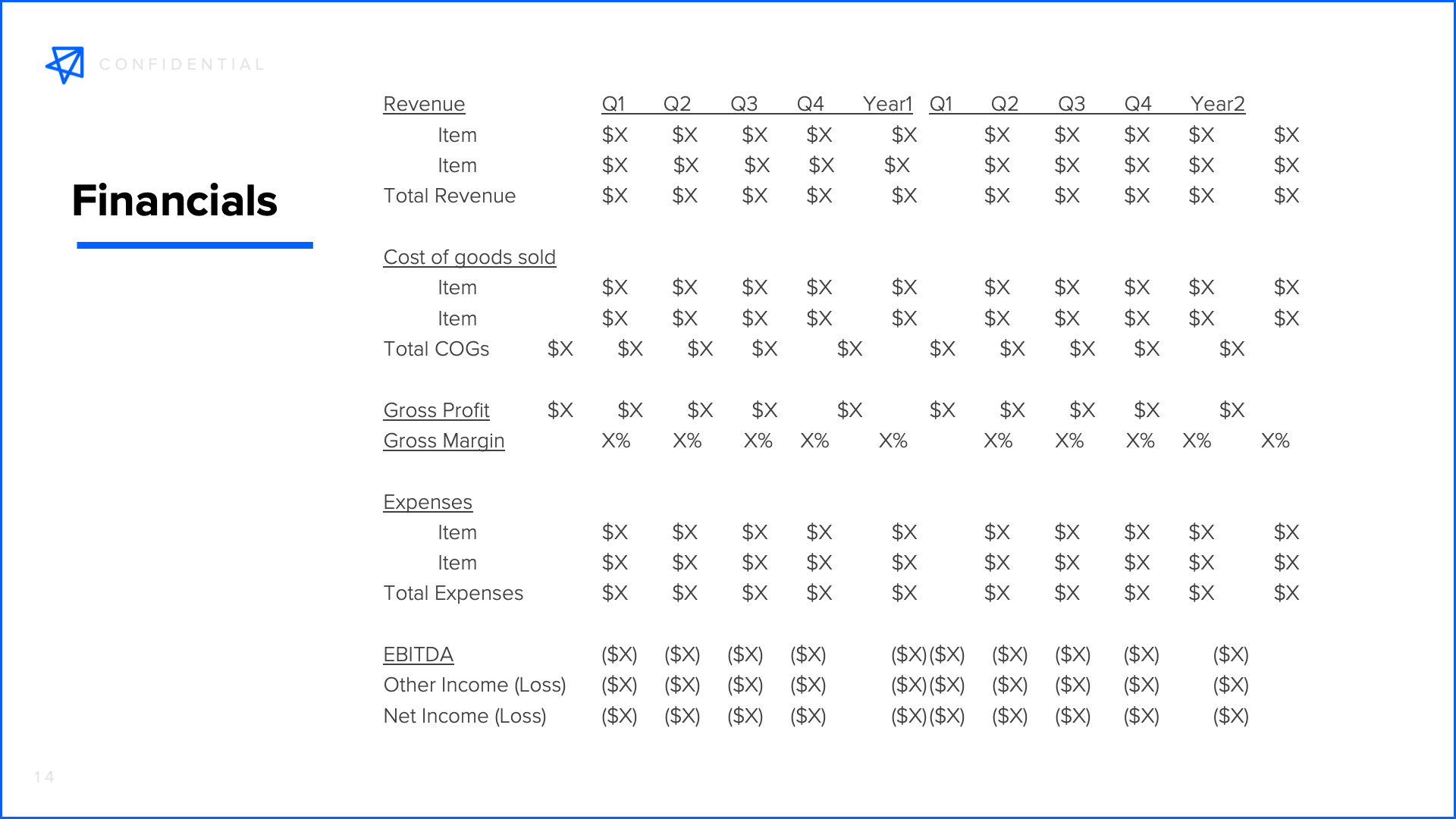

Financial Projections: At the seed how much a potential investor digs in to them differs, but nearly all investors want to see a set of financial projections. Of course all of the numbers will show the business going up and to the right – quickly! But the real significance of these figures is the exercise behind it.

Investors want to know the critical thinking behind the inputs and value-drivers of the business, and how that results in the outputs on the critical metrics and finances.

Product Snapshots: While some of the time there is an opportunity during a pitch meeting for a live demo, it’s not always the case. And often a deck is being read as a follow-up by the potential lead partner or the rest of her partnership. So screenshots of the key elements of the product can truly make the offering come alive that a mere description cannot.

It’s not a full substitute for seeing the product in real time, but including product images in an Appendix speaks to the team’s ability to execute and the crispness of the feature-set.

Traction Deep Dive: If you’ve got it, flaunt it. For “later” seed stage companies that have a business up and going, or even those earlier startups with some early market feedback, supplemental details about the market traction provide useful proofpoints about the venture.

Not only top-line growth in users or revenue, but also secondary numbers which speak to usage engagement and retention can instill confidence that the startups trajectory will continue after the next round of capital. There’s nothing like actual reality and accumulating momentum to help convince a new investor to jump on board the startup’s ship.

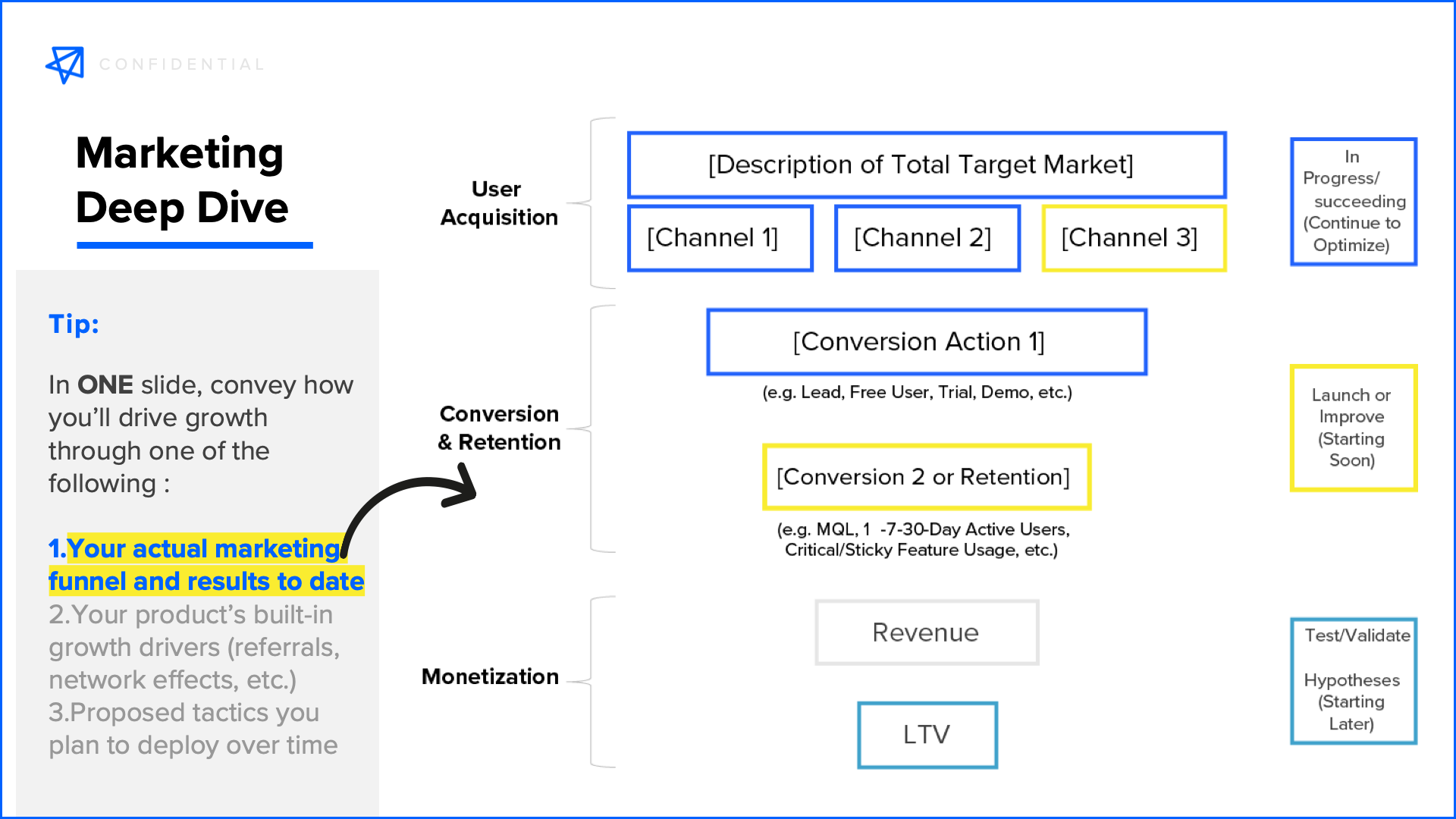

Marketing Deep Dive: How are you acquiring those customers and why? What channels have worked to date and done so cost-efficiently? How concrete is your understanding of each step in the marketing funnel? And perhaps most importantly, with addition of more capital, how will it be effectively spent to accelerate the business?

All of these questions can be addressed in an additional slide that take a closer look at the (sales &) marketing function of the organization and the results to date.

Other Questions: Every startup is different. Which is why each investor pitch is going to yield questions which are specific to that company. Just as an example, occasionally startups “rhyme” with previous failed attempts in a category by other startups, so it’s useful to proactively address the question, “Why hasn’t this worked in the past and why is it different this time?”

But whatever the bespoke topic, getting in front of a FAQs will demonstrate self-awareness about the challenges of the business and deliberate thoughtfulness about how to address them.

It’s OK for the Appendix section to be a “catch-all” of slides. But exhaustively including the various topics that a potential investor would want to know about allows for the core front section of the deck to be as concise and straightforward as possible. Nearly by definition, the

Appendix portion of the deck is unconstrained by length, as it’s a reference meant to be cherry picked in its usefulness. Once considered from this vantagepoint, the section can be used to a Founder’s advantage in covering topics that don’t always come up or don’t fit neatly into the main story but can serve as an important supplemental component in the pitch.