David Beisel

*This post is part of our “pitch deck” series where we dissect the seed stage pitch deck and discuss the ideal flow for a pitch. You can read the rest of the posts in the series by clicking here*

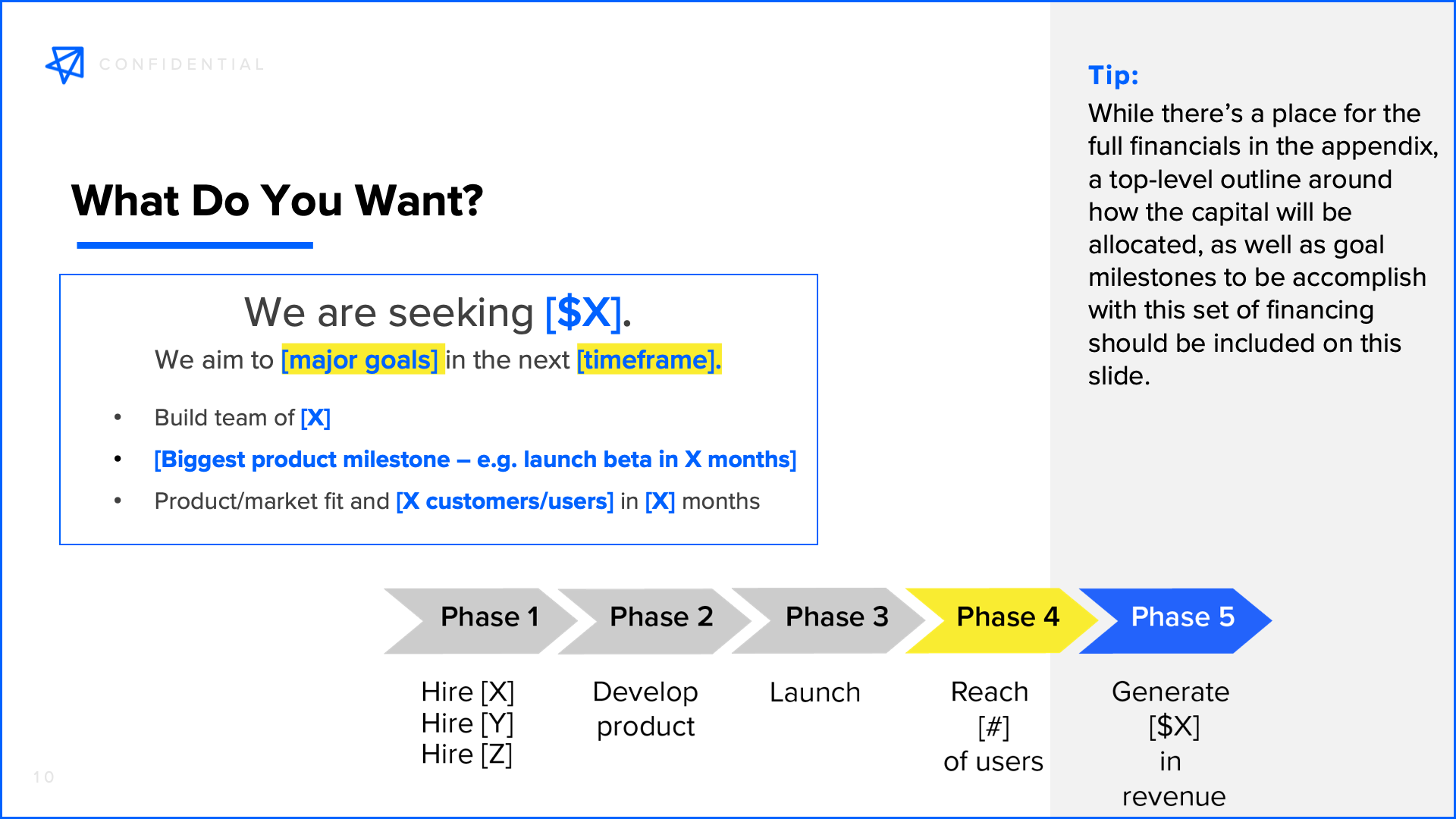

Here we are, at (one of) the final slides. The reason that you’re crafting the pitch deck, after all, is to raise funds. The closing slide of a pitch deck’s main section should be explicit about the ask. What do you want?

It’s to a Founder’s advantage to be up front & directly state how much capital you’d like to ideally raise in this round.

Personally, we prefer to share a (tight) range (e.g. $1.5m-$2m) rather than a specific figure. It shows some flexibility and allows for different investors (depending on their own fund size and strategy) to see a larger or smaller number depending on how they’d potentially fit into the round most easily. (Plus, it allows some wiggle room on being able to declare success even if the actual fundraising target isn’t reached.)

There are two other sets of information which should be included on the ask slide. First, it’s helpful to enumerate the startup’s funding history to date. To provide relevant perspective, listing past convertible note(s) and/or equity financing(s) including total round size and valuation (caps) is helpful.

Also, sharing some flavor (but not necessarily full detailed specifics) of the existing investor-set adds context. For example, stating “angels” is fine, and even highlighting notable names can be useful, but it’s unnecessary to share an exhaustive list. Previous venture firms’ specific involvement on the cap table should be noted here, though. Plus, any other non-standard items here should be called out, too, like non-dilutive grants, as applicable.

What not to include is directly stating valuation expectations. My partner Rob has previously written some thoughts on how to approach that conversation. In short, sharing pricing expectations early with potential lead investors fundamentally potentially qualifies your conversations, but it also runs the risk of prematurely losing a potential financing partner, or even reduce options to maximize your fundraise outcome. Regardless of what path to pursue, those expectations shouldn’t be written directly onto the slide, but rather felt out in a real-time face to face dialog.

The other set of information which we’d recommend including on this slide is what we call a stage roadmap. An entire slide in the Appendix section (to be outlined later) will be devoted to detailed financials projections. But it’s useful to include the expected inputs and outputs for the business over the next 12-18 months.

While there’s a place for the full financials in the appendix, a top-level outline around how the capital will be allocated, as well as goal milestones to be accomplish with this set of financing should be included on this slide. The former can include expected burn and runway, guideposts on hiring, and resource allocation.

The latter should simply state what this capital fundraise will “buy” you in terms of a few headline business proof points (e.g. develop and launch X product, reach Y number of users, generate $Z amount revenue).

The purpose of this ask slide is to demonstrate that you’ve given critical thought about the amount of capital which you’re raising, what you’re planning on doing with it, and what you will have to show for it as you’re approaching the need for another subsequent fundraising round. For a potential investor, it answers the questions of how much and why investing now is the right time.

Subscribe to our email list to get the posts delivered straight to your inbox, and have the final version waiting for you at the end of the month.